What’s driving me today isn’t what drove me in the past.

The time we’re living in right now is incredible, and I’m genuinely grateful to be part of it.

When I look back, there’s nothing I would change. The tough seasons, the setbacks, the pressure, that’s where the real growth came from. And today, my curiosity is higher than it’s ever been.

Despite everything I’ve learned, I still want to be the dumbest person in the room. I want to be surrounded by people who are smarter, sharper, and even younger. People who challenge me, push me, and expand how I think.

A lot of that perspective has been shaped at home.

My son Oliver, who’s five, inspires me every day. His curiosity, his energy, the way he sees the world, it’s powerful. It’s also a reminder of how much environment matters. Mary Elizabeth and I are intentional about protecting that, because at that age, everything leaves an impression.

The truth is, he’s teaching me just as much as I’m teaching him.

That mindset, that curiosity, it’s also what’s pushing me to give back to the community and ecosystem that’s been my professional home for over two decades.

Some of this may sound familiar, some of it may not, but I’d genuinely value your perspective.

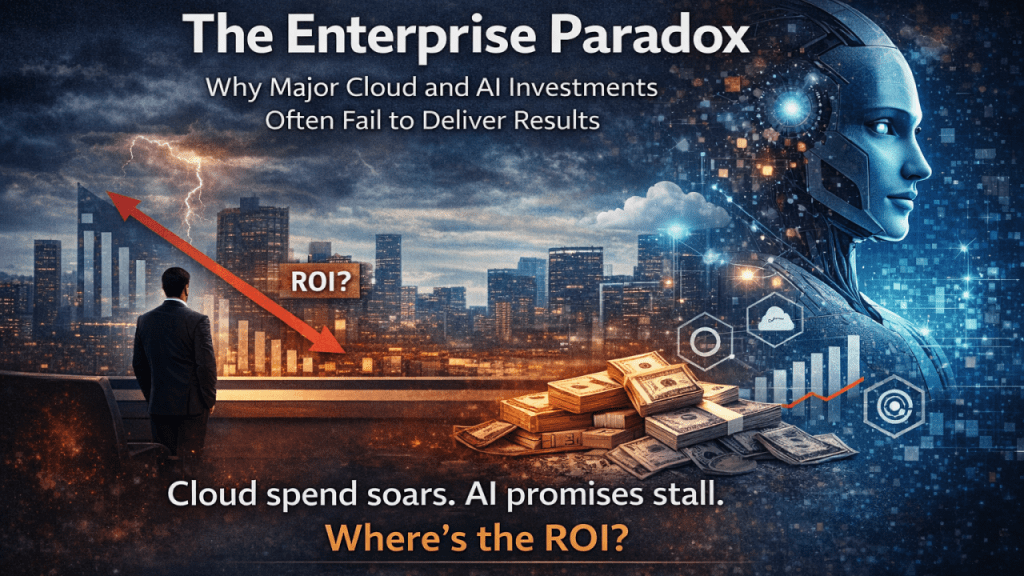

I wrote in my blog, “THE NEXT ERA OF ENTERPRISE TECHNOLOGY SERVICES: WHY SERVICE PROVIDERS MUST TRANSFORM NOW,” and one thing has become unmistakably clear.

The need for third-party expertise is not shrinking. It is growing.

But the expectations of that expertise are changing dramatically.

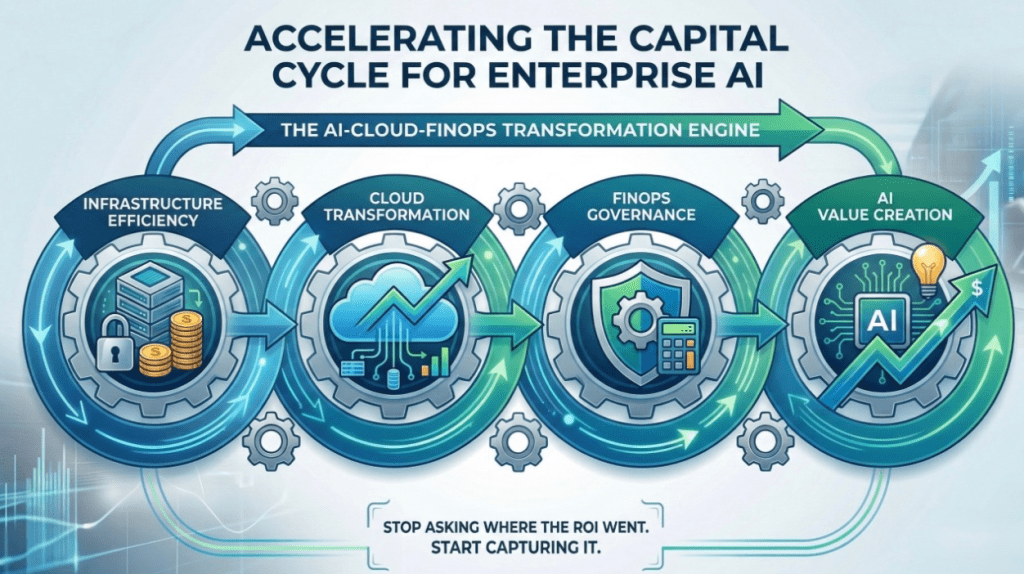

Enterprises are no longer looking for pure capacity or traditional outsourcing. They are looking for partners who can help them navigate complexity, orchestrate across multiple platforms, harness AI responsibly, and accelerate modernization outcomes with efficiency and precision.

This shift is redefining what it means to be a relevant and profitable player in the cloud and security services market.

I’ve always believed in the partner ecosystem. I believe in building highly technical teams and letting them run to drive innovation, growth, and value. I’ve always told my teams to embrace the partner channel, because it’s better to fish with a net than a pole. That has never been more true, especially as more revenue continues to flow through partners and marketplaces.

But here’s the conversation I keep having.

Every VAR I talk to right now is asking:

“Does AI kill our business model?”

No.

Buyer behavior didn’t change because of AI. It changed when cloud and marketplaces gave buyers options they never had before.

AI is simply accelerating what was already true.

And that leads to the real issue.

It’s the wrong question.

The right question is:

What do you need to stop doing?

Stop leading with implementation. You’re competing with hyperscalers who have scale you can’t match.

Stop getting overly dependent on resell. Keep it, but understand it’s the floor, not the ceiling.

Stop chasing AI use cases for clients who don’t have the foundation in place. You’ll build something that never makes it to production and wonder why it didn’t stick.

So what actually works?

Start with consulting and advisory. Be the person who tells the truth before a client spends millions in the wrong direction. That conversation is worth more than any implementation SOW.

Run workshops and enablement sessions. Your clients don’t need more technology. They need to know how to use what they already have. That is a paid engagement, not a free pre-sales activity.

Use AI to build new offerings. Not to replace your team, but to create leverage. A three-person team can operate like a fifteen-person team if done right. The firms that figure this out over the next 12 to 18 months will define the next decade.

Build an AI-first strategy, but don’t forget the fundamentals of cloud adoption, DevOps, FinOps, and the application development lifecycle.

So how do you actually become AI-first as a VAR, reseller, MSP, or channel partner?

Here’s the playbook.

From Benchmarks to Business Impact: Rethinking AI for Enterprise Adoption

Most AI evaluation today is academic. It does not translate to enterprise deployment, risk, or business impact.

If you want to lead in this next era, you have to close that gap.

1. Start with what’s broken Don’t start with AI use cases. Start with what’s not working. Use your experience to identify friction, waste, and missed outcomes. That’s where AI becomes relevant.

2. Fix evaluation before scaling AI What’s missing today:

- Trust

- Cost visibility

- Governance

- Model behavior in production

If you can’t measure it in the real world, you can’t scale it.

3. Make AI measurable in production Shift from model performance to business performance.

- How does it behave in production?

- What does it cost at scale?

- Where does it introduce risk?

- Does it actually change outcomes?

This is where real value is created.

4. Build with governance in mind AI governance is about to explode.

- Regulation is increasing

- Safety frameworks are evolving

- Enterprises are demanding accountability

This is not a constraint. It’s an opportunity.

5. Operate at the system level You’re not selling models. You’re designing operating models.

- How AI fits into workflows

- How it’s governed

- How it’s evaluated continuously

- How it scales across the enterprise

That’s where differentiation happens.

6. Bridge the gap others can’t Most AI companies build capability.

Very few understand:

- How it gets adopted

- How it fails in real environments

- How buyers actually think

That’s where you win.

7. Focus on outcomes, not experiments Enterprises don’t need more pilots. They need results.

Tie everything to:

- Cost reduction

- Efficiency

- Risk mitigation

- Speed

If it’s not tied to a business outcome, it won’t scale.

The outcome:

You move from vendor to advisor. You shift from projects to programs. You build recurring, high-margin services. You position your business at the center of how AI actually gets adopted.

This is the shift.

I close the gap between AI capability and real-world trust, adoption, and governance.

I operate at the system level, not the component level.

Because if you don’t connect evaluation to reality, you’re solving the wrong problem.

Some firms are already repositioning.

The ones waiting are already behind.

I’ve been having this conversation a lot lately. If you’re a VAR, reseller, GSI, or service provider trying to figure out where you fit in the next chapter, I’d welcome the conversation.

If this resonates, I’d value your perspective.